Investor spotlight: Managing risks when investing in German serviced apartments

By the time Pavel B. approached Tranio with an interest in investing in rental properties abroad, he was already an experienced commercial real estate investor. With a German supermarket and Greek flats under his belt, he was keen to expand his portfolio. But when we told him about a construction project in the German city of Aachen, he expressed some reluctance. He looked at the forecasted 10% annual return rate, and voiced concern that with high profits come high risks.

We reassured him that Tranio has the resources and experience required to mitigate some of these risks, and to ease his concerns. After digging further into the figures and research, he decided to move forward and is glad to have done so.

In this article, we explore Pavel’s investment, the risks at play, and what we did to help him mitigate these risks.

Tranio’s role in the project

We have been working in the international real estate market for 11 years and know first-hand how difficult it can be to find an investment project, and to confidently assess the associated risks. Using our network of connections, we support our clients at all stages of a transaction, shielding them against risks.

Contact us

The project: details and financial logistics

Tranio proposed this project to Pavel because while it offered high rewards, for various reasons we were confident in the risk calculus.

Taking shape in the city of Aachen, near Germany’s borders with Belgium and the Netherlands, these would be serviced apartments, i.e. fully furnished flats with hotel-like service offerings, such as room cleaning and laundry, which are available for short- or long-term rental.

The construction project was run by seasoned professionals. Overseeing the whole project is a developer with more than 40 years of experience, and upwards of 100 projects in its portfolio, including residences, retirement homes and serviced apartments. As is typical, the developer set up a project company to account for the financial flows related to the construction of the apartments in Aachen.

Furthermore, a subsidiary management firm had already agreed to rent the building as soon as it was completed at a set rate. This is, in fact, a standard practice aimed at risk reduction. Often, developers will seek renters for projects that have not yet been built to ensure minimal downtime once the property has been built. Typically in such scenarios, the renter begins paying rent and using the property immediately upon completion.

The management firm, a subsidiary of the developer, has been working with similar properties since 2016, and has wrought great success in the hospitality industry, as evidenced by its high rankings on Google and Booking.

The developer plans to sell the building upon completion in 2022, and having a rental agreement already lined up can be expected to increase its attractiveness to investors, and thus its price tag.

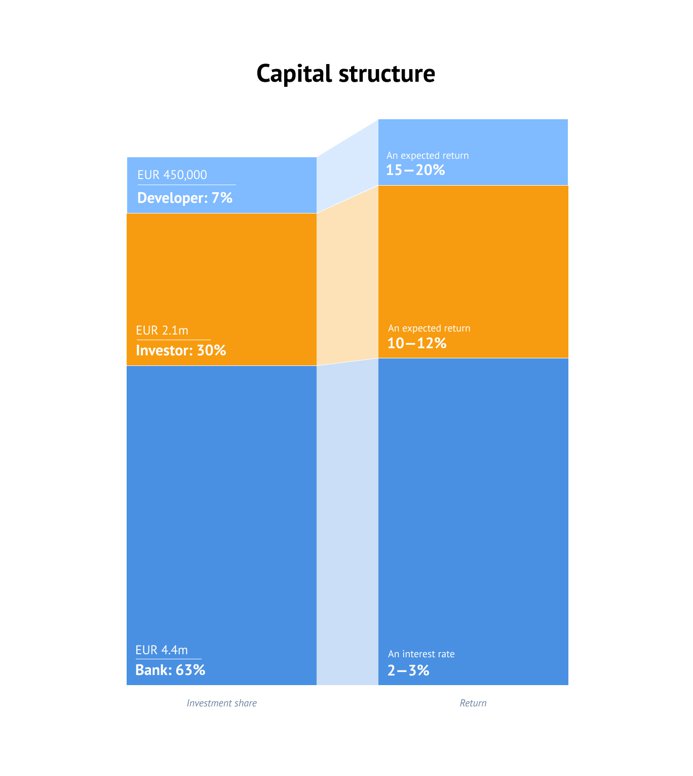

The budget breakdown for the EUR 6.9m construction project is as follows: EUR 4.4m was obtained via bank loans, while EUR 2.1m came from investors. The developer also contributed EUR 450,000 of its own funds.

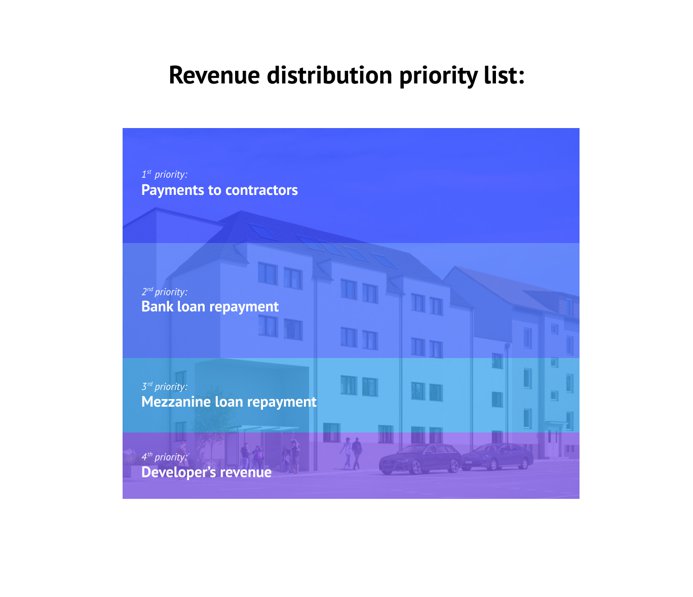

Pavel‘s investment in the project is what’s known as a mezzanine loan, a direct loan to the project company set up by a developer to build a facility. As loan repayments go, mezzanine loans fall third behind creditor payments and bank loans in the pay-out queue, while keeping priority over the equity. If the developer goes bankrupt, Pavel will get his money back after the developer pays off the loan to the bank.

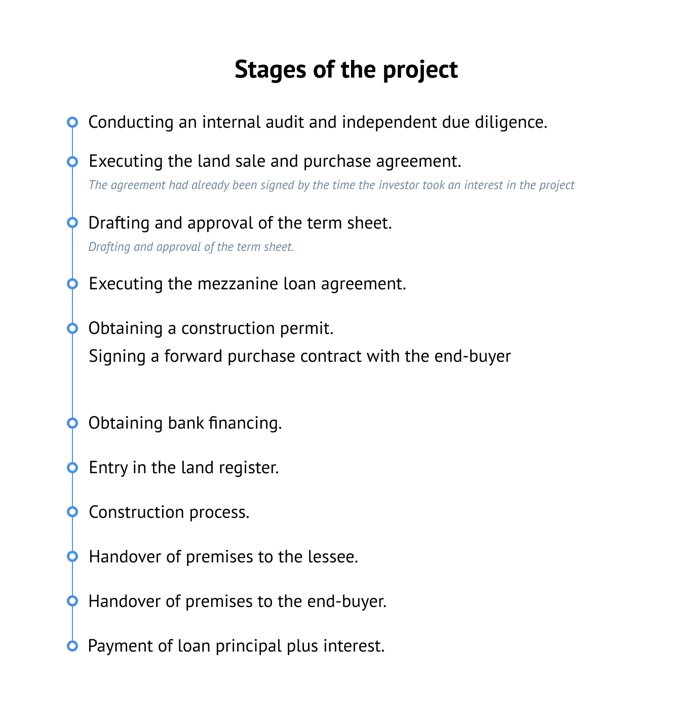

Project stages

By the time we proposed this project to Pavel, the developer had already signed a contract to purchase the land with deferred payment. The stages of the project are as follows:

Project risks

Risks may arise at any stage of a project like this one. Together with Pavel and the developer, we assessed the risks and offered solutions for each of them.

Risk #1: Missing out on a deal as a result of lost time and money

As developers and investors audit a project, someone else could swoop in and buy the land.

Mitigating factors: In this case, the developer had already signed a contract and paid an advance for the land, thus securing the deal. By putting its own money into the project, the developer showed its confidence in the project's success.

Risk #2: Construction permit denial

Local authorities sometimes refuse to issue a building permit, causing the project to be frozen or abandoned altogether, which can result in losses for investors.

Mitigating factors: In this case, the developer is so confident in its ability to obtain a permit that it is willing to provide a financial guarantee to the investor.

The German developer plans to obtain a building permit on the basis of §34 of the German Building Code, a common practice where the permitted building volume (height, project area) is assessed against the building volume of adjacent properties. Similarly sized buildings are already located next to the building site, proving that it is possible to obtain a permit for our site with the same dimensions.

To further reduce risk, we negotiated Pavel’s investment agreement to ensure he could transfer his investment in installments. At the time of the purchase, he deposited EUR 1.1m, with the understanding that he would pay the remainder after the building permit had been obtained. To further hedge the risk, we negotiated with the developer that if the building permit was not obtained within 18 months of the signing of the loan agreement, the developer would return the loan amount with interest.

Once a building permit is obtained, a land plot’s value increases. Thus Pavel is doubly protected; until a permit is granted, he has the developer’s guarantee, and once it has been granted, the plot will likely double in value. Even if something goes wrong, the developer can simply sell the plot at a profit and return the money to the investor.

Risk #3: Bank loan rejection

There is always a risk that a developer will be unable to secure bank loans for a project.

Mitigating factors: The investment contract included a clause stating that in the event the developer is unable to obtain bank financing within six months of signing, the investor has the right to withdraw the loan amount and accrued interest.

Risk #4: Unruly construction costs

There is always a risk that construction costs will exceed the budgeted amount.

Mitigating factors: The planned cost of construction for this particular project is about EUR 2,400 per square meter of usable floor space, which is below the market average. This is a standard construction project, and the developer has its own team of contractors, builders, architects and other specialists, which enables them to keep a lid on construction costs.

Nevertheless, construction cost overrun is one of the most common risks in the German market. To mitigate this risk for Pavel, we asked the developer to add a clause to the contract stipulating that in the event of a budget deficit, the developer is obliged to finance the deficit completely from its own capital.

Risk #5: The tenant will not be able to pay the rent

Once the project has been completed, there is always a risk that the future renter will be unable to pay as planned.

Mitigating factors: As mentioned above, Pavel entered the project with a rental agreement having already been signed.

To understand the severity of the risk that the renter will be unable to pay as planned, we analyzed the tenant-management company's revenue calculation to determine whether the rental rates are in line with the market. Half of the company's revenue is expected to come from long-term leasing and half from short-term leasing. We confirmed that their calculation were correct, and learned that the management company’s annual income (EUR 750,000) is more than double the building's occupancy fee (EUR 352,000). Ultimately, we were satisfied that even in the harshest of times, when, for example, short-term tenants are scarce, the company will have enough money to pay the rent.

Also, according to our calculations, the income per square meter of the building will be EUR 15 per month. This price corresponds to the market rates in Aachen. Let us assume that the management company renting the building is unable to pay the rent; in that case, the property can be rented out on a long-term basis to another operator. The profit from the lease would cover the bank loan payment.

Risk #6: Inability to sell

Another risk to consider is that of potential difficulties selling the property, which can be caused by market lulls.

Mitigating factors: As of the time of writing, the serviced apartments already have a potential buyer, but at the time of Pavel’s transaction, this had not been the case, and thus there was a risk that the property would not sell.

If the project had faced this obstacle, the property could have been rented out, the income from which would have covered the loan payment. In other words, even while waiting for better selling conditions, the property would generate a good return.

How we calculated the sales price

In Germany, a gross rent multiplier (GRM) is used to estimate the market value of a property, which shows the number of years the property would take to pay for itself through rental income. It is an indicator that is inversely proportional to the capitalisation rate. The market price of such a project is between 19 and 24 annual rental sums.

In our case, the building is expected to be sold for EUR 7.7m, with an anticipated rental income of EUR 352,000 per year; this 22x multiplier has already proven attractive, given that an interested buyer has already come forward. As mentioned above, the estimated construction cost of the facility was EUR 6.9m.

If we go back to our breakdown of equity shares (bank, Pavel, developer) and profitability percentages, we see that the difference from the sale of the facility will be more than enough to pay the revenues to all the participants, and the surplus is additional insurance against the risks.

Additional factors we took into account when determining the sales price:

- Aachen is a university town; half of the city center is occupied by the campus of Rheinisch-Westfälische Technische Hochschule Aachen (RWTH Aachen University). It is also home to the RWTH University Hospital, one of the largest in Europe. Given these factors, we are confident that students, visiting scholars, business affiliates of the university, medical workers and other professionals will be ensure ongoing interest in both short- and long-term rentals.

- Serviced apartments under construction qualify as residential properties, and residential properties are typically more expensive than commercial premises as they are considered to be less risky investments.

- In Germany, residential property cannot be rented out on a short-term basis without a license and permission from the municipality. In our case, the management company already has a license and permission. Half of the premises can be rented out on a long-term basis, which is reliable but less profitable, and half of them can be rented out on short-term bases, which is more profitable but carries the risk of downtime. However, even if all the premises are rented out on a long-term basis, we remain confident based on our calculations that the investment will pay off.

- Another difference between residential and commercial property is the legal designation of parts of the building. Whereas in a residential building you can obtain a cadastral number for each unit and sell it separately, in a commercial building the unit does not have separate documents and cannot be sold. In our case, it is possible to sell the units separately.

Thus, we believe that the project is attractive for the rental business and may be sold at or above the originally estimated price. But even in case of an untimely exit from the project, Pavel’s loan payment would be offset by rental income.

Exit from the project

The investor issued the mezzanine loan in December 2020, and by February 2021, an interested party had appeared who expressed a readiness to buy the serviced apartments before the construction completion. The actual transfer of the building to the new owner will take place upon its commissioning, but the contract with the buyer has already been signed. Pavel will get his money and interest back when the buyer transfers the money to the seller.

As with all of our clients, we were with Pavel each step of the way to ensure his investment was handled carefully and with an eye to maximal profits and minimal risks.

We will send you a content digest not more than once a week