German property market: 3 reasons why it’s insulated from a price crash

There is a universal opinion that the German economy is one of the most stable in the world, and German property prices growing steadily for the last eight years lends weight to the claim. But some experts, myself excluded, are claiming that the market is becoming overheated and that prices are set to fall. These experts are making the following arguments to support their claims:

- It is time for a new crisis: global crises happen about once in a decade, the last recession began in 2008, and a new one can be expected soon.

- Property is overpriced; the prices critically exceed rental dynamics: according to data from the Deutsche Bundesbank in 2017, property in the ‘Big Seven’ cities (Berlin, Hamburg, Düsseldorf, Cologne, Munich, Frankfurt and Stuttgart) was overpriced by 35%.

- Banking rates will soon rise: the European Central Bank has announced its intention to stop the asset buyout under the quantitative easing programme in late 2018. Experts expect loans to become more expensive, which is going to encourage residential property prices to fall.

In my opinion, this approach simply is not deep enough to allow proper insight into the problem, which further leads us down the wrong path to the wrong conclusions about the price fall. I believe the growth will continue but at a slower rate. Here, I’ll explain why.

A global crisis will not provoke a price decline

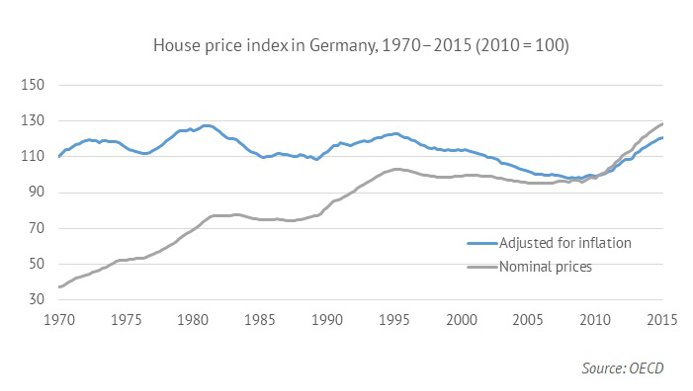

Even if a global economic crisis does happen, I believe it would not provoke a price crash. Over the past 50 years, three periods of recession have been observed in the German property market: in 1972–1976 (when residential property became 6% cheaper adjusted for inflation), in 1981–1989 (-15%) and in 1995–2008 (-20%). While the first two were provoked by the world crises of 1973 and 1979 with a 1–2-year delay, the third was related to residential property oversupply in the domestic market, meaning that after the 1990s there was an imbalance between German and other European markets. As the bubble burst in Europe and the US in 2007, Germany emerged relatively unscathed. Therefore, world conjuncture seems to have a limited effect on the property investment Germany.

German property has been growing in price since 2009 at approximately the same rates as in the first half of the 1990s. However, the current period of growth differs from the previous.

Firstly, price growth is currently supported by economic stability. During the first half of the 1990s, Germany's GDP was changing unevenly: from +5.3% in 1990 to 1.0% in 1993 and again +2.5% in 1994. Over the past 5 years, the economy has been growing and accelerating steadily: from 0.6% in 2013 to 2.5% in 2017. And the labour market behaved accordingly, when in the first half of the 1990s, the unemployment rate grew (from 5.5% to 8.2%), while between 2013 and 2017 it shrank (from 5.2% to 3.6%).

Secondly, there is not enough residential property at the moment. Similarly to the early 1990s, during the past five years, Germany's population has been growing at an approximately equal rate (about 450,000 people per annum), but the number of construction permits issued has shrunk annually, according to different estimates, by 1.5 –2 times. According to Thomas Bauer, President of the Central Federation of the German Construction Industry, Germany needs to build 400,000 residential units annually; the country issued 350,000 construction permits in 2017.

Thirdly, the structure of immigration has changed. In the 1990s, mostly refugees, immigrant labourers and repatriants were relocating to Germany; however, since 2010, there has been an influx of more professionals and academics among the arrivals. Many of them relocate under the EU Blue Card programme for well-educated professionals: according to data from Eurostat, Germany accounts for 85% of such permits.

The situation has changed especially significantly in Berlin, with its population growing by 50,000 people a year, with the total population standing at 3.5mn people. Most of the arrivals are young and middle-aged, well-educated, skilled workers. They come with money, wanting to rent and buy high-quality residential real estate. By doing so, they encourage residential property to become more expensive, adding 2–3 times greater pressure on its prices.

The difference between the acquisition value growth and the rental rates is overstated

An important feature that must be considered when comparing the price growth and rental rate dynamics is the overregulation of the real estate investment Germany. According to the rules, in three years an owner can raise the rent by no more than 20% (15% in Berlin), and in most regions, the landlord cannot increase the rent to a figure exceeding the official city rental index by more than 10%. Due to these restrictions, in large cities, the rental rate cannot grow as quickly as the purchase price formed by supply and demand mechanisms. Therefore, the data calculations based on the old rental agreements do not reflect the real demand, the population is ready to pay more. According to mortgage broker LBS, about 70% of residents rent apartments in Hamburg, and that number is 80% in Berlin. According to statistics from Immobilienscout24.de, there is an average of 77 potential tenants per apartment in Munich, 75 in Stuttgart, over 50 in Cologne and Freiburg and 33 in Berlin.

In July 2018, the German Institute for Economic Research (Deutsches Institut für Wirtschaftsforschung, DIW) published its ‘Signs of a new housing bubble in many OECD countries’ – lower risk in Germany’ report. DIW's experts analysed the OECD data on property price dynamics across 20 European countries and made two conclusions. Firstly, Germany is subject to lesser risk from the bubble than Sweden or the UK, for instance, thanks to the low levels of private household debt. Secondly, according to DIW's analysts, the German property market is overheated only in major cities, and, primarily in the newly-built apartment segment.

Mortgage rates not expected to grow significantly

Experts are not unanimous about whether the banking rates are going to increase; and if they do increase, when, how much and how quickly. In my opinion, there are currently no conditions for money to become significantly more expensive: the global economic slowdown has led to an absence of vehicles allowing to invest money with high returns in the modern world.

Moreover, the unlikelihood of a price crash in Germany due to more expensive borrowing is related to the features of the German mortgage market, which is very conservative. Local banks examine the borrower's solvency very thoroughly, and the LTV ratio rarely exceeds 70%. Therefore, a comparison of the existing situation with the 2008 U.S. mortgage market collapse is unfounded. Back then, banks were issuing 100% LTV loans to anyone who was interested, and when the borrowers were unable to pay the money back, and the banks began selling leveraged properties, property prices crashed. There was just nobody to buy this property.

In my opinion, German property prices will continue growing, though at lower rates. According to data from German consulting company Haufe, JLL has already been observing the first signs of the slowdown: as of H1 2018, apartment price growth rates in the eight largest German cities ran at 8.4% with the average of 9.7% over the past five years, 6.8% v 9.9% in Munich, 4.3% v 6.7% in Hamburg, while in Düsseldorf the growth practically stopped. However, I believe that there are no conditions for them to fall, while the German economy is developing in a way that favours the market: according to the European Commission’s forecasts, Germany's GDP is to continue growing by about 2% per annum. For the prices to begin falling, there must be urgent reasons: a surge in the interest rates or serious problems with the German economy, which is now one of the most stable and reliable in the world.

We will send you a content digest not more than once a week