Transnational real estate investment: 2021 year-end results of Tranio’s survey

- Cross-border property investors ramped up to or surpassed the pre-COVID-19 level of activity in most countries by the end of 2021.

- The countries offering residence permits or golden visa programmes saw the fastest rebound and market recovery, and the availability of online transactions was an additional growth driver.

These are the takeaways of Tranio’s tenth annual survey, conducted in late 2021 among 256 experts from 40 countries. The respondents shared their end-of-year recaps, forecasts and expectations for 2022.

Over the ten years that Tranio have been conducting market expert surveys, cross-border investors have gained more experience and developed stronger acumen.

Many of our clients already understand the rules of the investing game in the target market where they buy property, keep their yield expectations realistic, get surrounded by a team of advisors, and are on equal footing with local investors as a result. It was a rare case just a decade ago.

Golden visas facilitating market rebound

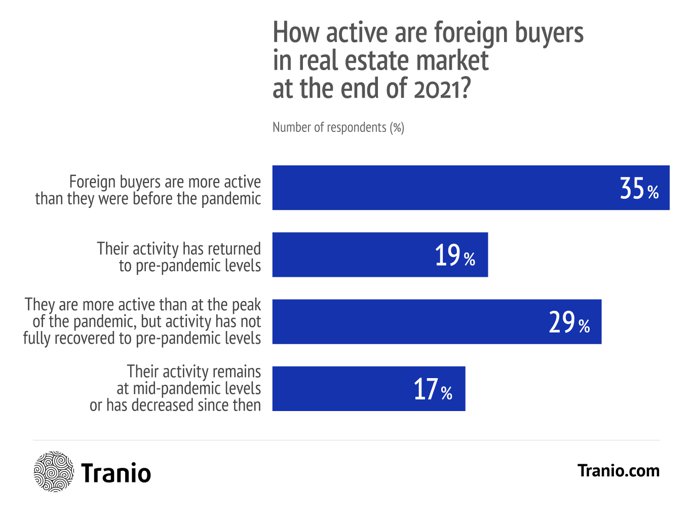

Over half of the respondents (54%) saw foreign buyers ramping up or surpassing their previous level of activity. However, 17% of those surveyed believed that by the end of 2021, the situation would be the same or even worse than it had been at the outbreak of the COVID-19 pandemic.

The countries that offer residence-by-investment programmes (golden visas in Spain and Greece, golden passports in Malta, etc.) saw a faster market rebound than those regions that have no similar programmes. 40% of respondents in the countries offering golden visas or passports, compared to just 28% in the other states, believe that foreign buyers have become more active than before the COVID-19 pandemic outbreak.

During the COVID-19 pandemic, many found it difficult to adapt to the mandatory travel restrictions, so investors showed more interest in the programmes and products allowing for freer international travel.

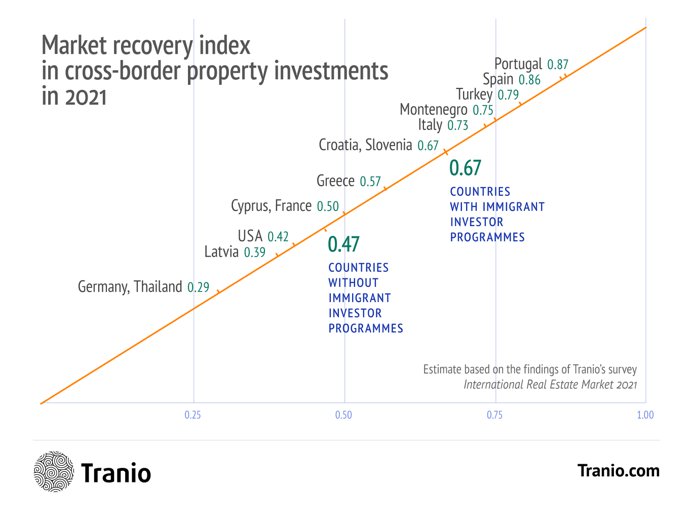

Based on the survey findings, we calculated the market recovery index for cross-border real estate investments in selected countries. The index value was set from 0 (if all the respondents chose the most pessimistic answer) to 1 (if all chose the most optimistic answer). Portugal reaches the highest market recovery index of 0.87, followed by Spain with an index of 0.86. Germany and Thailand close the list with an equal market recovery index of 0.29.

According to respondents in the Tranio survey, local buyers expressed more demand amid decreasing cross-border transactions in 2020–2021 in each of the countries reviewed.

All Tranio partners note increased interest from local buyers. Some of our partners targeting only foreigners before have now started to work with local clients as well.

It is still difficult to travel to other countries, yet money has to be invested somewhere so investors can tap into their local markets.

Average transaction value for housing at €354,000

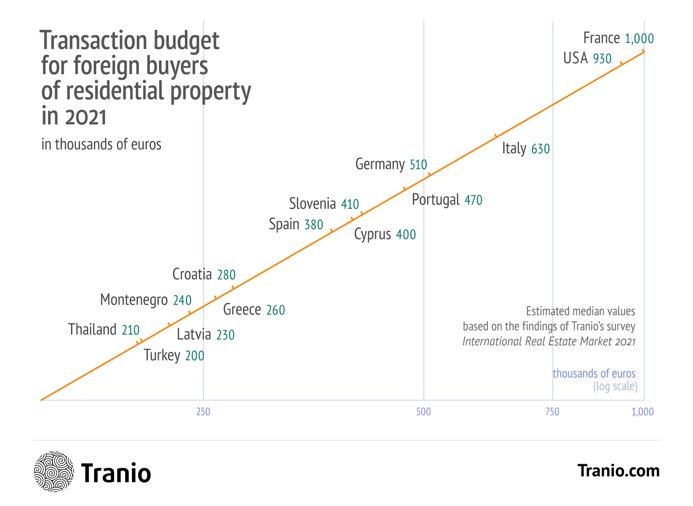

The survey findings allow for an estimation of the median budget of residential property sales by foreign buyers. The median budget averaged over all the reviewed countries amounts to €354,000, with material deviations in each state. Housing is the most expensive in France (with a median budget of €1,000,000) and the USA (€933,000), and the cheapest in Turkey (€200,000).

House prices and the market recovery index correlate: on average, the median budget is higher in countries where the markets bounce back better in 2021.

European buyers most active and clients from Russia and China outflowing

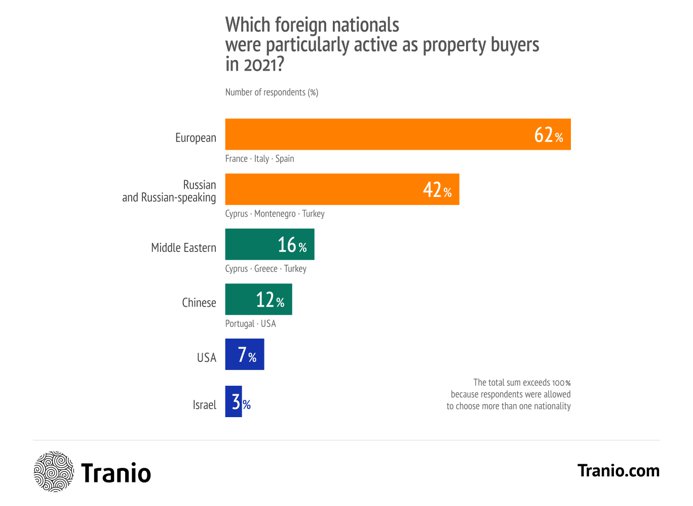

The majority of respondents (62%) believe that Europeans are the most active buyers acquiring property outside their home countries. This view is shared by 100% of respondents in France, 91% in Spain, and 90% in Italy.

The second most active in 2021 are buyers from Russia and the neighbouring C.I.S. countries (42%), followed by investors from the Middle East, China, the USA, and Israel. Some respondents note that market players from Canada, India, the Balkan States, Australia, Brazil, Egypt, and the SAR were also active.

Survey findings identified an interesting inter-country trend: the more active Europeans are said to be, the less active buyers from Russia and the C.I.S. are. This trend was most visible in Turkey, where 73% of respondents reported high activity from Russian buyers, while only 18% reported activity from Europeans. On the contrary, only about 17–19% of respondents in France, Spain, and Italy said buyers from Russia were active in the property market.

Property buyers from the Middle East stayed most visibly active in Turkey (55% of respondents), Cyprus (38%), and Greece (32%).

Investors from China were the top property buyers in the USA (71% of respondents) and the top three in Portugal (30%). US nationals were the top two buyers in Portugal (40%).

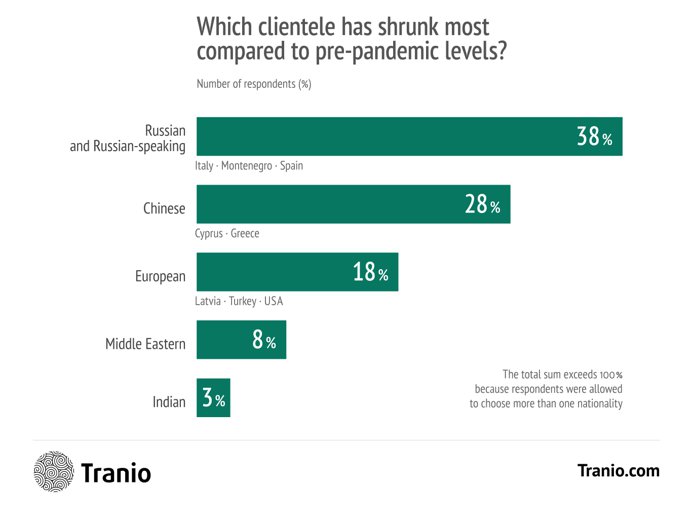

The most significant decline in cross-border investment activity by nation was among Russian and Chinese investors who were singled out by 38% and 28% of respondents, respectively. Nevertheless, some respondents reported a considerable outflow of buyers from Europe, the Middle East, and India.

The diminishing activities by Russian-speaking buyers were most marked in Spain and Italy (stated by 65% of respondents in each of the countries) and Montenegro (57%). Conversely, Russian-speaking buyers remained almost the same in Cyprus (the reduction is specified by only 8% of respondents) and in Turkey (by 9%).

Acquisitions by the Chinese declined sharply in Greece (noted by 61% of respondents) and Cyprus (50%). However, the business landscape was quite the opposite in the USA, France, and Montenegro, where not a single respondent noted the outflow of Chinese property buyers.

Property investment from Europeans declined the most in the Turkish market (marked by 64% of respondents), the USA (50%), and Latvia (40%).

There is a moderate degree of correlation between transaction value and the predominant investment choices of foreign buyers. The outflow of Russian and Chinese property buyers was most salient in the high-end foreign markets and was less evident in the affordable markets, whereas European buyers exited the affordable foreign markets in the first place.

As the outflow of foreign buyers in 2020–2021 was primarily connected with the COVID-19 restrictions, cross-border activities by buyers might be expected not just to bounce back but also to exceed the pre-pandemic level as the restrictions are lifted — the pent-up demand will revive the market.

Interest in golden visas grows most strongly in Portugal and declines in Latvia

In 2021, the average number of investors willing to obtain a golden visa or passport in the countries offering such programmes rose by 1.2 times in comparison to the previous year. According to our respondents, Portugal stands out among the offering states, with the average interest in the residence-by investment programme doubling compared to the year 2021. Portugal is followed by Montenegro with a 1.5-fold increase over the same period of time.

As of 2022, Portugal no longer issues residence permits for investments into residential properties in coastal locations, including Lisbon and Porto.

The Montenegrin golden passport programme was expected to be suspended in late 2021, but was extended until the end of 2022 at the last moment.

So investors had to speed up property acquisitions in both countries, seizing the moment when the programmes were still valid as before.

According to the survey participants, interest in golden visas did not develop only in two countries in 2021: Cyprus retained the level of the previous year, and interest in Latvia went down by 38%.

Interest in golden visas and the market recovery index are reported to be tightly interconnected, which upholds the underlying assumption that residence permits and golden visa programmes helped the market to navigate through the crisis.

Online transaction availability facilitating market recovery

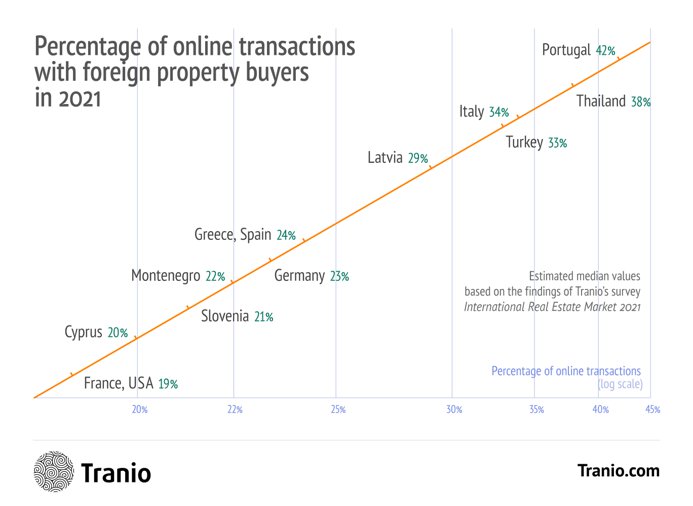

International travel restrictions have brought about a growth in online transactions. The survey respondents estimate that foreign property buyers closed an average of 23% of transactions online without visiting the country of property acquisition in 2021. Portugal leads the way again, with online transactions making up 42% of the overall breakdown.

Our clients buying rental apartments now more often tend to close transactions remotely rather than in person in the country of purchase.

Newly developed apartments in districts with high rental yields are almost all sold out at the earliest construction stages when there is nothing to look at on the construction site.

The number of remote acquisitions correlates with the market recovery index. This leads us to the assumption that the availability of online transactions, in addition to golden visas, is yet another driver of cross-border sales.

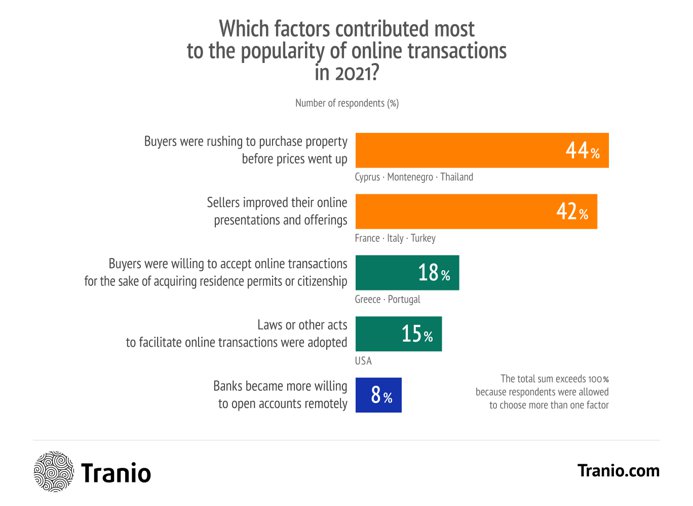

Other factors, alongside border closures, boosted online transactions in 2021. In particular, 44% of respondents say that buyers opted for a remote transaction because they were willing to buy real estate before price growth. Another 42% of respondents note that sellers have been more actively using digital to show properties by conducting e-viewings or filming drone videos of properties.

Fear of price hike is thought to be the main motivation for online transactions in Thailand (reported by 100% of respondents), Montenegro (83%), and Cyprus (78%), whereas the importance of a digital property show is noted especially in France (80%), Turkey (64%), and Italy (61%).

Most survey participants in Portugal (67%) believe that remote property purchase gained traction as clients made acquisitions to obtain residence permits. This survey option also tops the list in Greece, chosen by 44% of respondents.

About 80% of all Tranio clients who bought their properties remotely in 2021 were looking for golden visas or golden passports.

The property market rebounded faster in 2021 in countries where sellers were more actively showing their properties online. This conclusion is underpinned by the strong correlation between the responses about online transaction drivers and the market recovery index.

Property market players optimistic about the future

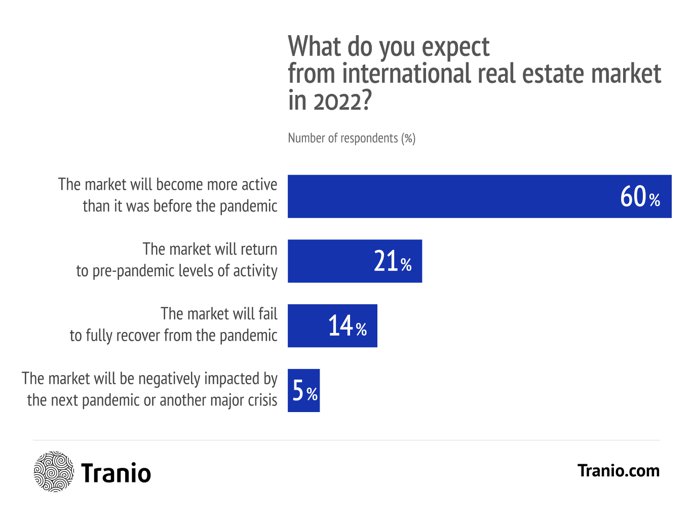

60% of respondents believe that the international property market would be more active in 2022 than before the COVID-19 pandemic. 68% of respondents anticipate this in the countries offering golden visa programmes.

We expect that the balance in sales of different types of property will be tipped as the property market recovers. For example, investors in short-term rentals would now be looking more often for long-term rental properties.

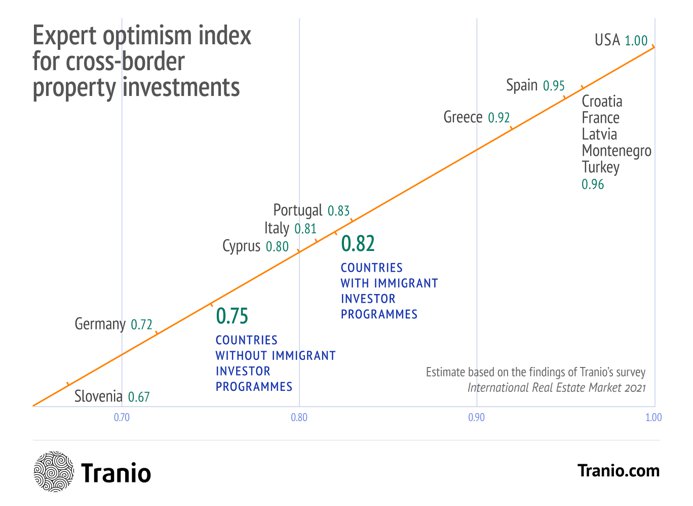

Similar to the market recovery index, we have calculated the expert optimism index in the cross-border property investment market of the selected countries, showing expectations for the 2022 market. The optimism index has a maximum value of 1 in the USA, where 100% of respondents believed in the best-case scenario at the end of 2021. The optimism index exceeds 0.67 in all countries except Thailand, where 40% of respondents anticipate another pandemic or yet another severe crisis in 2022.

Similar to the market recovery index, we have calculated the expert optimism index in the cross-border property investment market of the selected countries, showing expectations for the 2022 market.

The optimism index has a maximum value of 1 in the USA, where 100% of respondents believed in the best-case scenario at the end of 2021. The optimism index exceeds 0.67 in all countries except Thailand, where 40% of respondents anticipate another pandemic or yet another major crisis in 2022.

We identified a correlation between the expert optimism index and online transaction drivers. The expert optimism index is higher in countries that facilitate online transactions through laws or other state measures. However, it is lower in countries where banks are more willing to open accounts remotely.

I believe the online transaction trend is here to stay for the long term. Many investors acquired investing know-how to choose counterparties and make major investment decisions and will be keeping up this business acumen after the COVID-19 pandemic.

We will send you a content digest not more than once a week